Discovering The Financial Journey: What Is The Net Worth Of A Juvenile?

It's a curious thought, isn't it? When we talk about someone's financial standing, we usually picture adults with careers and investments. But what about younger folks? What does it truly mean to consider the net worth of a juvenile, and why might that even be a topic worth exploring? It's a bit like looking at a sapling and imagining the mighty tree it could become; the early stages, you know, they really do matter for what's ahead.

For many, the idea of a child having "net worth" seems a little strange, perhaps even a bit much. Yet, as we've seen in other discussions, even complex systems, whether they're about how software updates keep things running smoothly or how a young person's financial habits start to form, often have foundational elements that are worth looking into. This isn't about making kids feel like tiny CEOs, though. It's really about understanding the building blocks of financial literacy and how early habits can shape a person's money story for years to come.

This article will shed some light on what net worth looks like for someone young, why it matters, and how families can help foster a healthy financial outlook from an early age. We'll talk about what goes into a young person's financial picture, and perhaps, just perhaps, you'll see that it's more than just pocket money and birthday gifts. It's about setting a course, you know, for a lifetime of good money sense.

Table of Contents

- What is Juvenile Net Worth, Really?

- Why Does a Juvenile's Net Worth Even Matter?

- Components of a Young Person's Financial Picture

- Building Good Money Habits Early On

- Common Questions About Juvenile Finances

- The Role of Guardians and Mentors

- Legal Considerations for Young People's Money

- Looking Ahead: Financial Futures

- Conclusion: Nurturing Financial Growth

What is Juvenile Net Worth, Really?

When we talk about net worth for an adult, it's usually the total value of everything they own minus everything they owe. So, it's like, your house, your car, your savings, your investments, all that good stuff, minus your mortgage, credit card bills, and other debts. For a young person, the concept is pretty much the same, but the scale and the types of items involved are quite different. It's a simpler picture, in a way, but still meaningful.

A juvenile's net worth is, you know, the sum of their assets—things they own that have value—minus their liabilities—what they might owe. This could include money in a piggy bank, a savings account, perhaps some small investments like a few shares of stock gifted by a grandparent, or even valuable possessions they might own. On the other side, liabilities for a young person are usually pretty minimal, perhaps a small loan from a parent for a toy they really wanted or money they promised to pay back for something. It's a snapshot, really, of their current financial standing.

This idea, in some respects, isn't about counting every single toy or gadget. It's more about understanding the flow of money, the idea of ownership, and the very early stages of financial responsibility. It's a way, you know, to introduce the basic concepts of money management without making it too complex. Think of it as a first step on a very long financial path.

Why Does a Juvenile's Net Worth Even Matter?

You might be thinking, "Why bother with the net worth of a child?" And that's a fair question. The truth is, it's not about the dollar amount itself, but what the exercise of understanding it teaches. It's about planting seeds for future financial health, you see, and that's pretty important.

Teaching young people about their net worth, even in a simplified way, helps them grasp fundamental financial principles. They learn about assets, which are things that put money in their pocket or hold value, and liabilities, which are things that take money out. This basic understanding is, you know, a crucial building block for making smart money decisions later in life. It's a very practical lesson, actually.

Furthermore, it helps foster a sense of responsibility and ownership. When a young person understands they have a "financial picture," however small, they might be more inclined to save, to think before spending, and to consider the future. It's about empowering them, in a way, to take control of their own financial journey, even if it's just with their allowance money right now. This approach, you know, can really make a difference as they grow up.

Components of a Young Person's Financial Picture

So, what exactly goes into figuring out the net worth of a young person? It's typically a much simpler calculation than for an adult, but it still follows the same logic of assets minus liabilities. It's, you know, a pretty straightforward equation, all things considered.

Assets for Young People

For a young person, assets can include a few different things that hold value. These are the positive parts of their financial picture, you might say. What could those be, you ask? Well, there are some pretty common examples.

- Cash Savings: This is probably the most obvious one. Money in a piggy bank, a savings jar, or a bank account set up for them. This is, you know, their most liquid asset.

- Custodial Accounts: Many young people have accounts like a UGMA (Uniform Gifts to Minors Act) or UTMA (Uniform Transfers to Minors Act) set up by parents or grandparents. These accounts can hold cash, stocks, bonds, or mutual funds, and are managed by an adult until the child reaches a certain age. They can be quite significant, actually, for a young person's future.

- Investments: Sometimes, young people might directly own a few shares of stock, perhaps gifted to them or purchased with their own saved money through a custodial account. Even small amounts can, you know, start to add up over time.

- Valuable Possessions: While not always included in a formal net worth calculation for kids, items like a valuable collection (stamps, coins, rare cards), a musical instrument, or even a high-quality bicycle could be considered assets if they hold significant resale value. This is, you know, a bit more of a gray area, but still worth thinking about.

- Gift Cards: Unused gift cards can also be seen as a form of asset, as they represent future spending power. They're, you know, like a pre-paid mini-fortune.

It's interesting to consider that even small things, when looked at from a financial perspective, can contribute to a young person's overall financial standing. It's not always about big numbers, you know, but about understanding what has value.

Liabilities for Young People

Compared to adults, liabilities for young people are usually pretty simple and, frankly, often quite small. They don't typically have mortgages or car loans, you know, which is a good thing!

- Loans from Family: This is the most common type of liability. A young person might borrow money from a parent or guardian for a specific purchase, like a new video game or a concert ticket, with an agreement to pay it back from future allowance or earnings. This is, you know, a great way to teach about debt.

- Small Debts to Friends: Occasionally, a young person might owe a friend a small amount of money for lunch or a shared activity. These are usually short-term and minor, but still count, you know, in a casual sense.

The key here is that liabilities for juveniles are generally very manageable and often serve as early lessons in the concept of debt and repayment. It's a safe space, in a way, to learn about financial obligations.

Building Good Money Habits Early On

Understanding net worth is one thing, but actively helping young people build positive financial habits is where the real impact happens. This is, you know, where the rubber meets the road, so to speak. It's about practical steps that can really make a difference.

Allowances and Earnings

Providing an allowance is often the first step in a young person's financial education. It gives them their own money to manage, which is, you know, a big deal for them.

- Regular Allowance: A consistent allowance teaches budgeting and planning. It's their money to manage, and they learn to make choices about spending and saving. This consistency, you know, really helps them get a handle on things.

- Earning Opportunities: Beyond allowance, offering opportunities to earn money through chores, odd jobs for neighbors, or even starting a small, age-appropriate business (like lemonade stands or pet-sitting) can teach the value of work and entrepreneurship. This is, you know, a very valuable lesson.

These experiences, whether from an allowance or earned money, provide a safe environment for young people to experiment with financial decisions and, you know, learn from their choices.

Saving and Spending Strategies

Helping young people differentiate between wants and needs, and encouraging thoughtful spending, is pretty vital. It's, you know, a skill that serves them well their whole lives.

- The "Save, Spend, Share" Jar System: This classic method helps young people allocate their money into different categories. A portion goes to saving for a bigger goal, some for immediate spending, and a bit for charitable giving. It's a very visual way, you know, to teach allocation.

- Goal-Oriented Saving: Encourage saving for specific items they want. When they save up for something they really desire, they learn patience and the reward of delayed gratification. This is, you know, a powerful motivator.

- Smart Spending Choices: Talk about making informed decisions. Compare prices, look for value, and discuss whether a purchase is truly worth it. These conversations are, you know, incredibly helpful.

These strategies help young people develop a mindful approach to their money, which is, you know, a key component of financial wisdom.

Introducing Investing Concepts

While formal investing might seem too complex for young people, introducing basic concepts can be incredibly beneficial. It's about, you know, planting the idea early.

- Compounding Interest: Explain how money can grow over time, even small amounts, thanks to compounding interest. Use simple examples, like a savings account that earns a little extra money each year. This concept is, you know, truly powerful.

- "Owning a Piece of a Company": If they have a custodial account with stocks, explain that they own a tiny part of a company. Talk about companies they recognize, like a favorite toy maker or a tech company. This makes it, you know, much more relatable.

- Long-Term Growth: Emphasize that investing is for the long haul. It's not about getting rich quick, but about steady growth over many years. This perspective, you know, is really important for future success.

These early introductions can demystify investing and make it less intimidating as they get older. It's a gentle way, you know, to open up a whole new world of financial possibilities.

Common Questions About Juvenile Finances

People often have a lot of questions when it comes to young people and money. Here are a few common ones, you know, that often come up:

How can a child earn money legally?

Young people can earn money through various legal avenues, depending on their age and local regulations. This often includes allowances for chores, gifts, and informal jobs like babysitting, pet-sitting, or yard work for neighbors. For older teens, part-time jobs in retail or food service are common, but there are usually specific rules about working hours and types of work they can do. It's, you know, all about finding age-appropriate opportunities.

What's the best way to teach kids about saving?

One of the most effective ways to teach kids about saving is by setting clear, achievable goals. Help them identify something they really want, like a new toy or a special outing, and then work with them to save a portion of their allowance or earnings towards that goal. Using clear jars labeled "Save," "Spend," and "Share" can also be a very visual and effective tool. This approach, you know, makes saving tangible and rewarding.

Are there special bank accounts for minors?

Yes, there are indeed special bank accounts designed for minors. These are typically custodial accounts, such as a Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA) account, which are opened and managed by an adult (the custodian) for the benefit of the minor. The money belongs to the child, but the adult controls it until the child reaches the age of majority (usually 18 or 21, depending on the state). Some banks also offer joint accounts where a parent is a co-owner, which can be a good way to introduce banking basics. It's, you know, a safe way to start their banking journey.

The Role of Guardians and Mentors

Parents, guardians, and other trusted adults play a really important part in shaping a young person's financial understanding. They are, you know, the primary educators in this area.

It's about more than just giving money; it's about providing guidance, setting examples, and having open conversations about money. Talk about your own financial decisions, both good and bad, in an age-appropriate way. Explain why you make certain choices, like saving for a big purchase or paying bills on time. This transparency, you know, can be incredibly valuable.

Mentors can also help young people learn about the world of work and money. Whether it's a family friend who owns a business or a teacher who runs a financial literacy club, these figures can offer different perspectives and practical advice. They can, you know, show them different paths and possibilities. The goal is to create a supportive environment where financial questions are welcome and learning is encouraged, which is, you know, pretty essential for growth.

Legal Considerations for Young People's Money

When it comes to money for young people, there are some legal aspects to consider, especially as their assets grow. This is, you know, where things can get a little more formal.

Custodial accounts, like UGMA and UTMA, are common ways for adults to hold and manage assets for minors. These accounts have specific rules about how the money can be used (it must benefit the minor) and when control transfers to the child. It's important to understand these rules to ensure compliance and proper management. For instance, once the child reaches the age of majority, they gain full control of the assets, which means, you know, they can do what they wish with it.

For young people who earn income, there are also tax implications. Depending on how much they earn, they might need to file a tax return. This can be an early lesson in civic responsibility and understanding the tax system. It's, you know, a part of growing up financially. Consulting with a financial advisor or tax professional can be helpful for families with significant assets or earnings for young people, just to make sure everything is handled correctly. You can learn more about custodial accounts on our site, and also find information on tax implications for minors.

Looking Ahead: Financial Futures

The concept of a juvenile's net worth is really about laying a strong foundation for their financial future. It's not about creating child millionaires, you know, but about fostering smart habits.

By understanding what assets they have and how to manage them, young people can build confidence and competence in handling money. These early lessons, however small, can prevent future financial struggles and set them on a path toward financial independence. It's about empowering them, you know, to make good choices for themselves.

As they grow, their financial picture will naturally become more complex, involving things like student loans, first jobs, and bigger investments. But the groundwork laid in their younger years—the understanding of saving, spending, earning, and even the very idea of net worth—will serve as a valuable guide. It's, you know, a journey that starts with small steps but leads to big possibilities.

Conclusion: Nurturing Financial Growth

Exploring the net worth of a juvenile isn't about numbers on a spreadsheet for a child; it's about the powerful lessons embedded within those numbers. It's about teaching our younger generation the fundamental concepts of financial responsibility, asset building, and thoughtful money management. By introducing these ideas early on, through practical experiences like allowances, goal-oriented saving, and even simple discussions about what things cost, we're doing something truly important.

The goal is to equip young people with the confidence and skills they'll need to navigate their financial lives as they grow. Every small step, from understanding a piggy bank balance to learning about a savings account, builds a crucial foundation. So, let's keep nurturing these vital financial conversations, because empowering young people with money wisdom is, you know, one of the best investments we can make in their future. It's a journey, for sure, and it starts right now.

Juvenile Net Worth - Net Worth Post

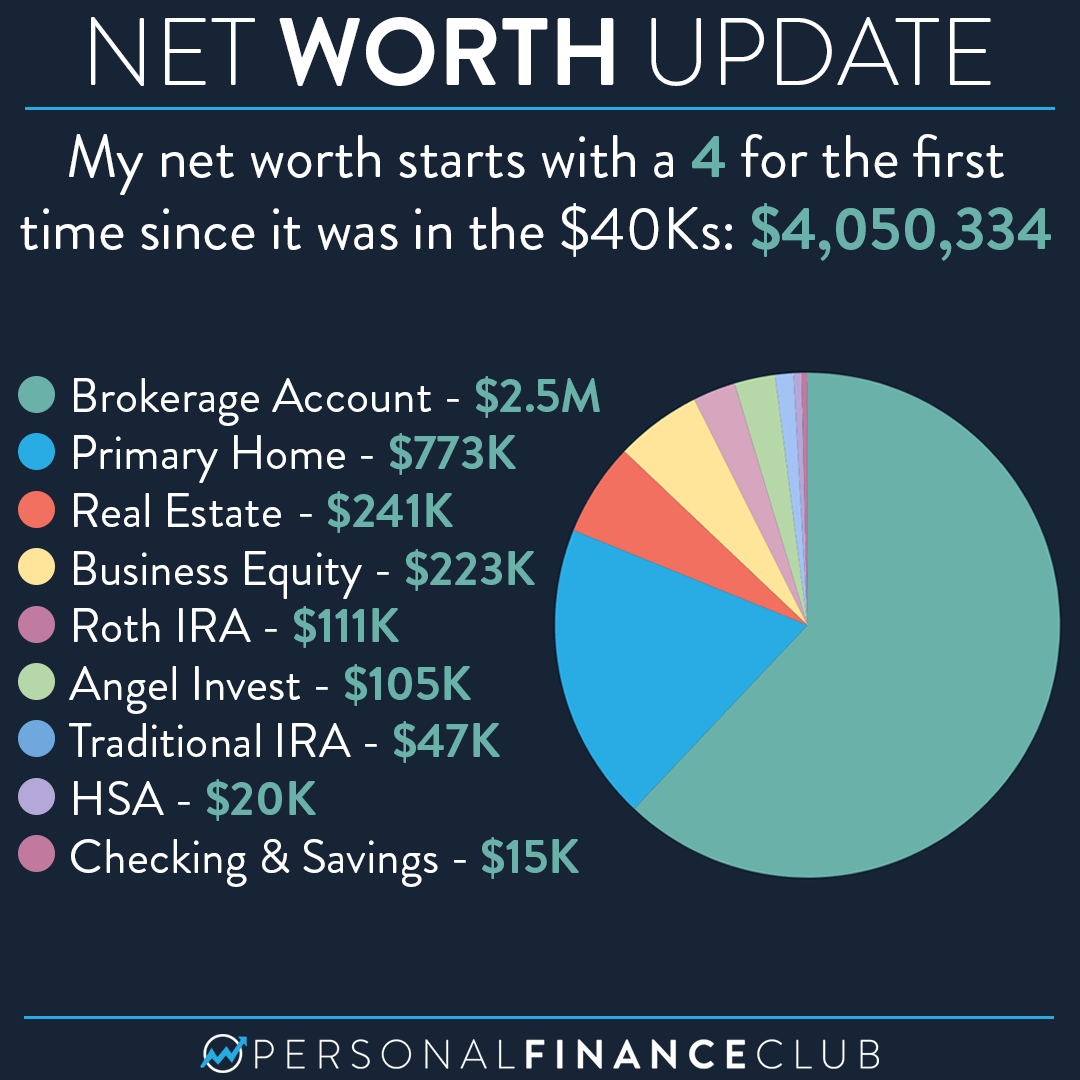

My $4 million net worth breakdown! – Personal Finance Club

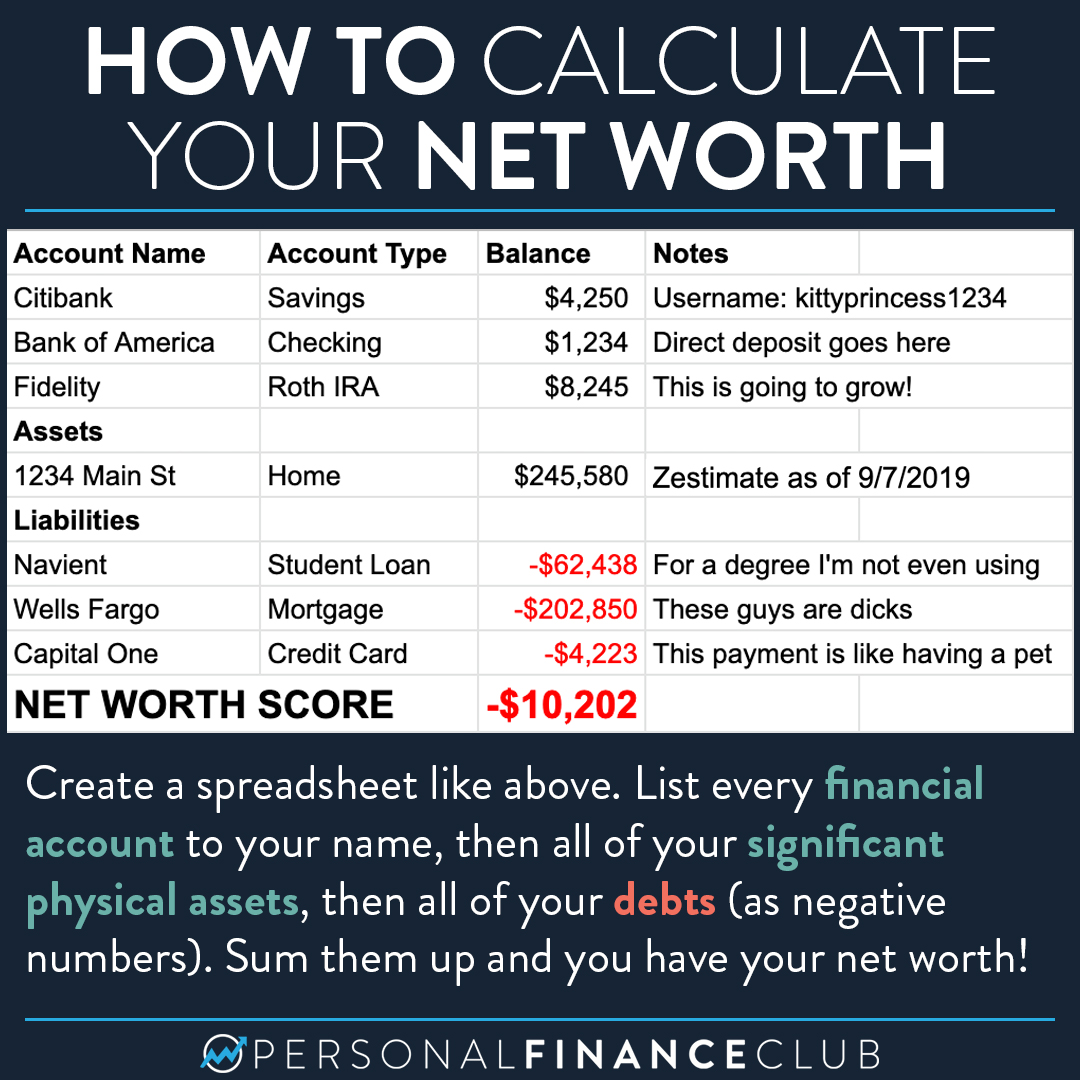

How to calculate your net worth – Personal Finance Club